If you lend to SSMEs in Nigeria, this applies to you.

Most loan decisions are made with limited visibility. No solid records. No dependable credit history. Yet approvals still happen. That gap is where losses come from.

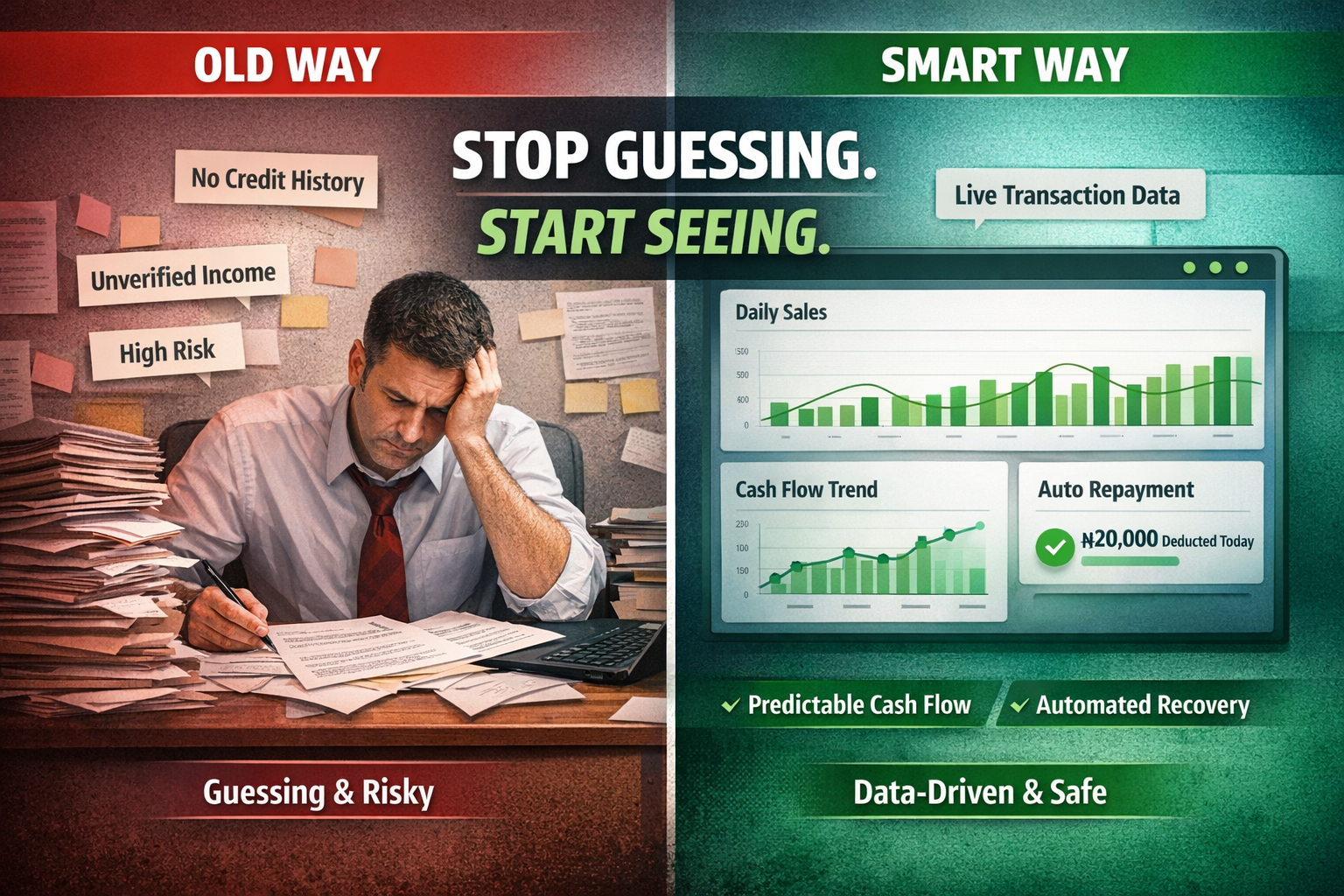

There is a more practical approach already in use by companies like Nomba. It is built around one idea: use real business data, not assumptions.

1. Check What the Business Earns, Not What It Says

Before approving any loan:

Pull recent transaction history

Focus on actual inflows over the last 8–12 weeks

Working rule:

Only lend a portion of weekly turnover, not the full amount.

2. Prioritise Consistency Over Big Numbers

High revenue can be misleading if it is unstable.

Look for daily or near-daily sales, predictable income pattern, no long gaps in activity. Consistency reduces uncertainty.

3. Collect Repayment as Sales Happen

Waiting for fixed repayment dates creates pressure.

A better approach is to deduct small amounts from daily sales and align repayment with cash flow.

4. Start Small, Then Scale

Avoid large exposure at the beginning.

Issue smaller first loans

Increase only after proven repayment behaviour

This limits early-stage risk.

5. Track the Business Continuously

Do not rely on one-time checks.

Monitor sales trends, transaction frequency, and growth direction. This keeps your risk assessment current.

What This Changes

Better loan decisions

Reduced default rates

Faster turnaround time

Less reliance on collateral

Final Thought

If you are a lending company, your biggest advantage is not more capital.

It is better visibility into the businesses you fund.

And today, that visibility is already in the data.